The Memory Crisis Is Splitting the Smartphone Market Into Two

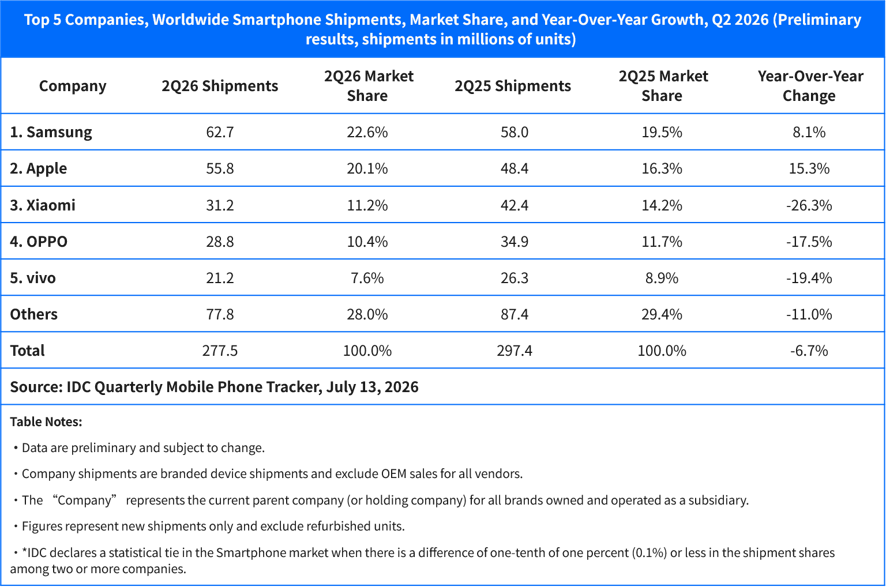

Global smartphone shipments fell to 277.5 million units in the second quarter of 2026 — a 6.7% year-over-year decline and the second consecutive quarterly drop, according to preliminary data from IDC’s Quarterly Mobile Phone Tracker released Tuesday.

Memory costs are the root cause. DRAM and NAND prices have climbed nearly 300% compared to a year ago, and in low-end devices, memory now accounts for more than 65% of the total bill of materials. That math doesn’t work for brands that depend on volume.

“It completely confirms what we predicted — this downturn is not uniform across the market,” said Nabila Popal, IDC’s senior research director for global consumer devices. “The memory crisis is benefiting premium brands and crushing vendors that rely on low-end models.”

The result is a market splitting into two distinct tiers.

On one side, Apple and Samsung — the only two vendors in the top five that grew shipments for a second straight quarter. Apple posted a record Q2, driven by strong iPhone 17 series demand and consumers buying early ahead of expected price increases. Samsung expanded its market share by 3.2 percentage points. Apple gained 3.8.

IDC’s analysis suggests Apple’s full-year market share could hit 22%, an all-time high.

On the other side, every Chinese OEM in the top five — Xiaomi, OPPO, vivo — saw double-digit declines. Xiaomi’s drop was the steepest, but IDC characterized it as strategic: the company is deliberately cutting low-end volume to protect margins and shift into higher price tiers.

Francisco Jeronimo, IDC’s vice president for global client devices, said the divergence between premium and budget segments intensified sharply in Q2. Apple and Samsung locked in memory supply early, and memory represents a smaller share of their overall BOM anyway. That gives them room that low-end competitors simply don’t have.

“The issue is not the strategy itself,” Popal said. “It’s whether consumers will accept higher-priced products from brands they’ve traditionally associated with budget devices. When the price gap narrows and installment plans are available, they tend to gravitate toward premium brands.”

Huawei was the outlier, posting 20.9% year-over-year growth. The company held prices steady while Android rivals raised theirs, ran targeted promotions, and leaned on strong domestic brand loyalty. A broader product portfolio covering more price points helped.

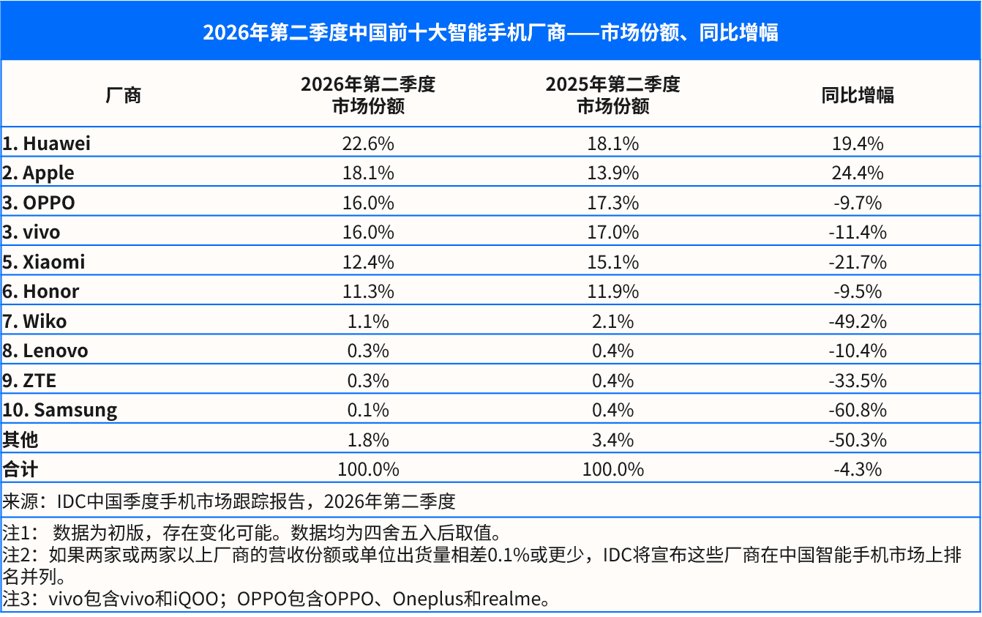

China’s smartphone market — the world’s largest — shipped approximately 66 million units in Q2, down 4.3% year-over-year. That’s the fifth consecutive quarterly decline. Android vendors began raising prices or adjusting configurations in late March as component costs climbed, which visibly suppressed upgrade demand.

The “618” shopping festival, traditionally a mid-year sales peak, saw overall smartphone sales drop nearly 15% compared to last year.

Kiranjeet Kaur, IDC’s associate research director for global consumer devices, noted that Chinese OEMs still depend on the sub-$200 market for volume. Several are refreshing old models or even reviving 4G variants to hold that price band while cutting costs elsewhere.

The outlook is grim for the second half. IDC expects China’s smartphone market to contract by roughly 20% year-over-year in H2 2026 as vendors burn through the last of their low-cost memory inventory and face the full force of current pricing. The report sees no meaningful relief from high memory prices in 2027.

But Popal offered one note that rings true: consumers haven’t stopped needing phones. They’re just holding onto them longer. When the replacement cycle finally turns — IDC expects that around 2028 or 2029 — demand will come back. The question is which brands will still be standing to meet it.