Storage Costs Are Crushing the Budget Smartphone Market

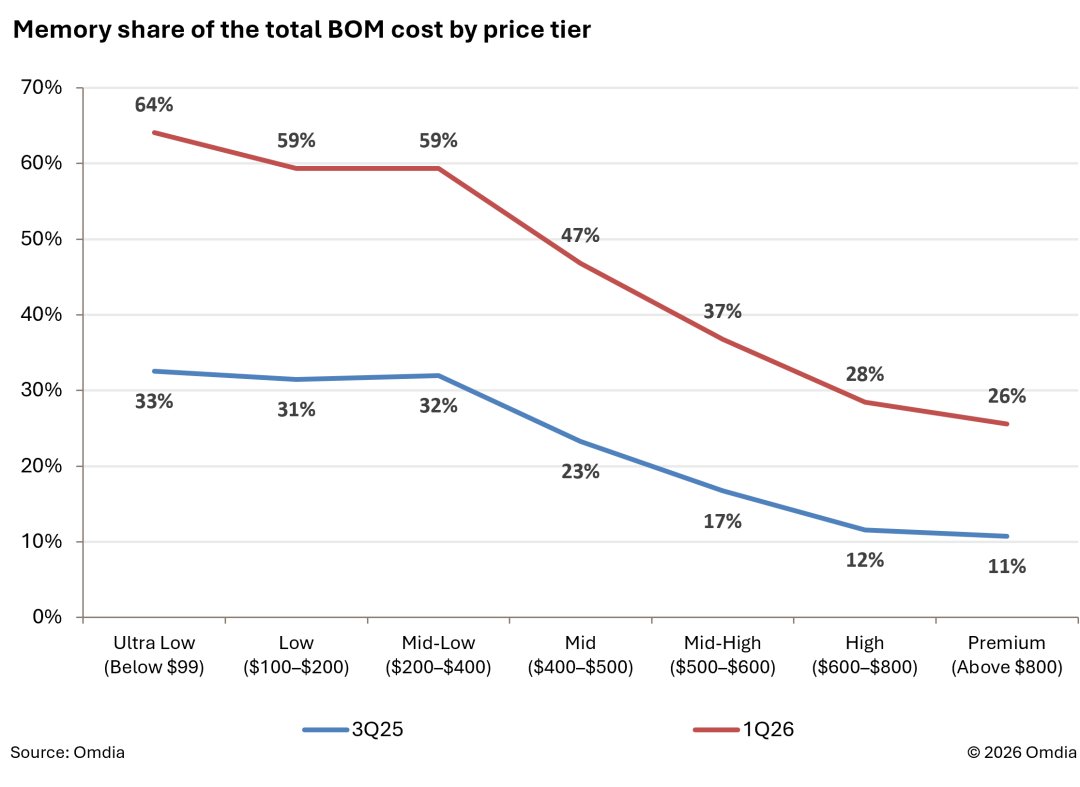

The numbers are stark. DRAM and NAND prices have been climbing for several quarters now, with no relief in sight, and the segment of the phone market that can least afford to absorb those increases is taking the hit. According to Omdia’s latest research, storage’s share of the bill of materials in sub-$400 smartphones nearly doubled in the first quarter of 2026. The result: the sub-$400 market is contracting by more than 22 percent year over year.

For price-sensitive buyers, even a modest retail price increase is enough to kill a purchase. Phone makers know this, and they’re quietly pulling back from the low end rather than trying to eat the rising costs. Omdia forecasts that global smartphone shipments will decline 12 percent overall in 2026, and the entire drop is concentrated in the budget tier. The above-$400 segment, by contrast, is expected to grow 5.7 percent.

The mechanism is straightforward. In a sub-$400 phone, storage has become one of the largest single line items on the BOM. When memory prices double — and Omdia’s data shows they’re on track to keep rising — the math on a low-margin device stops working. Manufacturers either take a loss, raise the price and lose customers, or downgrade components elsewhere to compensate.

They’re doing a bit of all three. On the component side, Omdia flags several strategies taking shape across the industry. Chinese phone makers are switching from LTPO OLED panels back to LTPS OLED in mid-range models, saving an estimated $3 to $5 per device. On cameras, they’re using smaller sensors or cutting the number of rear lenses. And on processors, they’re stretching older-generation SoC platforms longer — using last year’s chip instead of the latest one can cut silicon costs by 30 to 40 percent.

Above $600, the picture is different. Storage still costs more, but it accounts for a much smaller share of the total BOM because the SoC, display, and camera modules in flagship phones are dramatically more expensive. A high-end phone has more margin to absorb memory inflation, and its buyers are less sensitive to price increases in the first place.

The underlying trend — memory prices climbing while phone volumes sag — isn’t new, but the speed of the shift has caught the industry off guard. DRAM and NAND suppliers have been disciplined about capacity expansion after the last downturn, and AI demand has pulled a growing share of high-bandwidth memory supply away from the consumer market. Budget phones are stuck in the squeeze.

Omdia expects the sub-$400 market to keep shrinking through at least the end of 2026. Phone makers that built their business on volume — the brands that ship tens of millions of entry-level devices a year — are being forced to choose between margin and market share.